The year 2025 marked a defining chapter in the history of the Nairobi Securities Exchange (NSE). After several years of subdued performance, weak foreign participation, macroeconomic stress, and valuation compression, Kenyan equities staged a powerful and broad-based recovery. Major indices delivered returns exceeding 50%, market capitalization crossed historic thresholds, and investor confidence—particularly among local investors—returned decisively.

Yet, while headline numbers suggest a uniform rally, the reality beneath the surface was more nuanced. The 2025 market was highly concentrated, sector-driven, and selective at the stock level. Banking stocks dominated returns, dividend-paying companies regained relevance, and liquidity gravitated toward balance-sheet strength rather than speculative growth stories.

As we move into 2026, the market landscape is evolving again. Valuations are no longer distressed, interest rates appear closer to a plateau, and future returns are likely to be lower, steadier, and more dependent on earnings and dividends rather than valuation re-rating alone.

This article provides a comprehensive review of the NSE’s 2025 performance and a forward-looking investment outlook for 2026, covering:

- Market and macroeconomic context

- Sector-by-sector performance analysis

- Top-performing and underperforming stocks

- Dividend yield expectations for 2026

- Portfolio construction implications for Kenyan investors

Macroeconomic and Market Context of 2025

From Stress to Stabilization

The NSE entered 2025 following a challenging macroeconomic period. Elevated interest rates, fiscal pressure, currency volatility, and declining foreign investor participation had weighed heavily on equity valuations in prior years. By late 2024, many blue-chip stocks were trading at multi-year valuation lows, dividend yields were historically elevated, and investor sentiment was deeply pessimistic.

What changed in 2025 was not a dramatic economic boom, but rather stabilization:

- Inflation moderated

- Interest rate expectations peaked

- Currency volatility eased

- Corporate earnings began to recover

This shift from uncertainty to predictability proved sufficient to trigger a powerful re-rating of Kenyan equities.

NSE Market Performance in 2025

Index-Level Performance

The NSE delivered one of its strongest annual performances in recent history:

- NSE 20 Share Index: ↑ ~56%

- NSE All Share Index (NASI): ↑ ~51%

- NSE 25 & NSE 10 Indices: ↑ ~50%+

Market capitalization surpassed KSh 3 trillion, reflecting significant wealth creation for investors who remained invested or re-entered the market early.

Note: Index performance alone does not tell the full story; sector-level analysis provides the real insight.

Sector Performance

1. Banking Sector: The Engine of the 2025 Rally

The banking sector was unequivocally the primary driver of NSE returns in 2025, delivering average gains of approximately 60–70%.

Why Banks Outperformed:

- Improved asset quality and lower credit provisioning

- Strong loan growth despite a high-rate environment

- Recovery in fee-based income

- Dividend reinstatement and increases

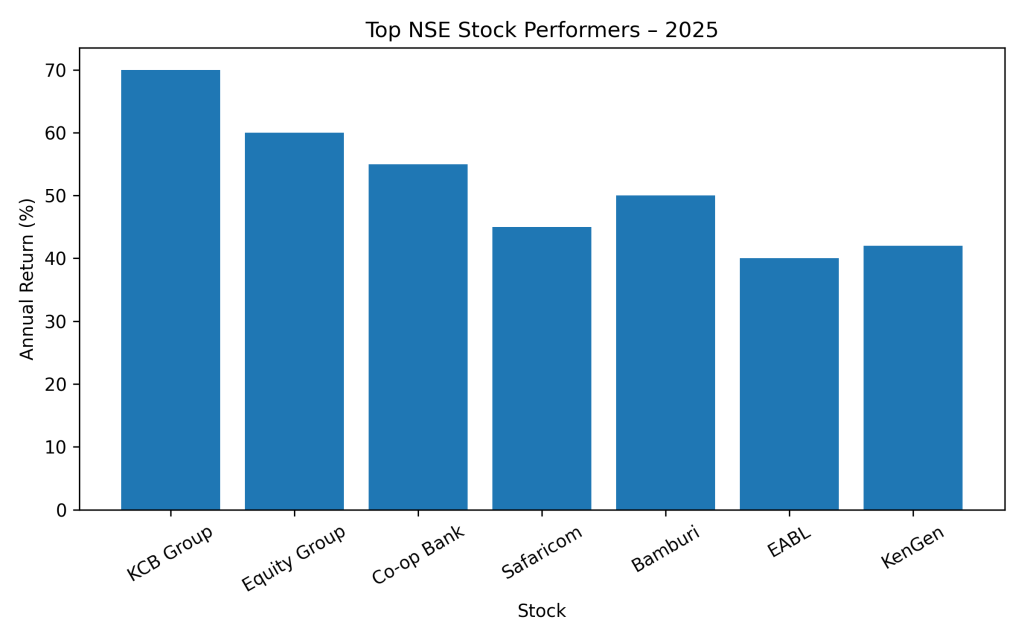

Major beneficiaries: KCB Group, Equity Group, Co-operative Bank.

Banks offered a rare combination of:

- Attractive valuations

- Improving fundamentals

- High and growing dividends

Institutional investors, particularly pension funds, favored banking stocks as the natural destination for capital.

2. Telecommunications: Defensive Stability in a Volatile Market

The telecommunications sector—effectively represented by Safaricom—delivered solid but more measured gains of approximately 40–50%.

Key drivers:

- Resilient cash flows

- Continued growth in M-Pesa and data revenues

- Defensive characteristics in a still-fragile macro environment

While not the top performer, Safaricom played a critical role in portfolio stabilization and income generation.

3. Energy and Utilities: A Partial Recovery

Energy and utility stocks experienced a moderate recovery in 2025 after years of underperformance.

Example: KenGen benefited from:

- Normalization of power demand

- Improved revenue visibility

- Relative policy stability

However, structural risks—particularly government receivables and regulatory uncertainty—continued to limit valuation upside across the sector.

4. Manufacturing and Industrials

Manufacturing and industrial stocks gained approximately 30–40% in 2025, supported by:

- Lower financing costs

- Infrastructure-related demand

- Improved margins as FX pressures eased

Examples: Bamburi Cement, EABL

These companies benefited from both cyclical recovery and pricing power.

5. Insurance: The Quiet Underperformer

Despite improving fundamentals, insurance stocks lagged the broader market in 2025. The sector’s underperformance was driven by:

- Thin liquidity

- Limited retail participation

- Preference for banks within financials

This underperformance may lay the foundation for a valuation catch-up in 2026.

6. Agriculture: Defensive but Challenged

Agricultural stocks delivered modest returns of around 20–25%, constrained by:

- Weather variability

- Input cost inflation

- Export market volatility

Agriculture offered diversification benefits but remained a tactical rather than core allocation.

Stock-Level Analysis – Winners and Losers of 2025

Top Performing NSE Stocks

Performance was concentrated among a relatively small group of liquid, fundamentally strong companies.

Notable winners:

- KCB Group: Strong earnings rebound and attractive dividend yield

- Equity Group: Regional diversification and balance-sheet strength

- Co-operative Bank: Consistent profitability and income appeal

- Safaricom: Defensive growth and cash generation

- Bamburi Cement: Cyclical recovery

- EABL: Margin improvement and brand strength

Common characteristics of winners:

- Strong balance sheets

- Predictable earnings

- Dividends or dividend recovery

Underperformers and Laggards

Stocks that lagged typically suffered from:

- High leverage

- Regulatory uncertainty

- Weak liquidity

- Structural business challenges

Utilities with heavy government exposure and illiquid small-cap stocks remained under pressure despite the broader market rally.

2026 Outlook – Growth with Structural Support

1. Bullish Momentum Likely to Continue

The NSE entered 2026 with momentum still on the upside. Early January index readings remained elevated (e.g., NSE 20 over 3,140). Analysts expect continued market capitalization expansion and price appreciation, especially among large-cap and mid-cap counters.

2. New Listings and Market Depth

Anticipated new listings in 2026 could deepen the market and drive further investor interest:

- AA Kenya

- Kenya Pipeline Company (KPC) — potentially IPO’d by Q1-Q2 2026

- Family Bank

These new listings are expected to attract both local and foreign capital.

3. Continued Structural Enhancements

- Single-share trading and financial literacy initiatives will likely boost retail investor participation.

- Policy focus on privatizations and IPOs (e.g., KPC and other state assets) could add new capital market entry points.

4. Risks and Considerations

- Foreign investor participation has been weaker, making the market more reliant on domestic liquidity.

- Institutional capital, like pension funds, remains under-deployed, creating potential volatility if large inflows occur suddenly.

Dividends Return to Center Stage in 2026

Why Dividends Matter More Now

With equity valuations significantly higher after the 2025 rally, future returns are expected to be more dependent on earnings and dividends than on price appreciation alone.

Supporting factors:

- Interest rates are stabilizing

- Pension funds favor predictable cash flows

- Retail investors increasingly seek income stability

Expected Dividend Yield Outlook for 2026

High Dividend Yield Candidates:

- Co-operative Bank: ~8–10%

- KCB Group: ~7–9%

- Equity Group: ~6–8%

- Safaricom: ~6–7%

- EABL: ~5–6%

- BAT Kenya: ~9–11% (with structural risks)

Dividend sustainability, rather than headline yield alone, will be critical.

Conclusion: From Rally to Resilience

The NSE’s performance in 2025 marked a decisive break from years of underperformance. The rally restored investor confidence, re-established equities as a viable asset class in Kenya, and rewarded discipline over speculation.

Focus now shifts from capital gains to cash returns, from valuation recovery to earnings durability, and from momentum to portfolio resilience.

The Exchange delivered an exceptionally strong 2025 performance, driven by broad-based equity gains, structural reforms, and improving investor confidence. As 2026 unfolds, the market appears well-positioned to continue growing — supported by new listings, enhanced participation, and stable macroeconomic trends — though vigilance around foreign flows and institutional investment trends will remain key to sustaining momentum.

{kind=link}