The 2007–2008 financial crisis and the global recession that followed were the most severe economic events since the Great Depression of the 1930s. The crisis did not arise from a single mistake or an isolated shock. Instead, it was the result of a complex interaction between macroeconomic forces, financial innovation, regulatory gaps, and institutional incentives that collectively encouraged the creation and widespread distribution of high-risk assets.

Across the financial system, risk was willingly assumed and passed along—from households taking on large mortgage debts, to financial institutions structuring mortgage-backed securities, to global investors purchasing these instruments with borrowed money. As long as U.S. house prices continued to rise, the system appeared stable and profitable.

When housing prices finally began to fall, however, this highly leveraged financial structure collapsed. The decline exposed how deeply interconnected the system had become and how dependent it was on ever-rising asset prices. In hindsight, the sequence of events and the links between them are clear. At the time, however, the sheer complexity of the system—and the number of participants involved—meant that few observers fully understood the scale of the risks being accumulated or the magnitude of the crisis that was unfolding.

Home Purchase Options and Residential Mortgages

When individuals seek to purchase a home—an asset that typically costs several times their annual income—they generally face two options:

- Save a substantial portion of their income over many years until they can afford to buy a home outright. For most households earning an average income, this approach would delay home ownership until their forties or fifties, even with disciplined saving.

- Borrow money. By taking out a loan—usually from a commercial bank—buyers can purchase a home immediately and repay the borrowed amount, plus interest, through regular monthly payments over a long period, typically 25 to 30 years. This type of long-term loan is known as a residential mortgage and has historically been the primary mechanism through which households access home ownership.

Traditionally, banks followed what is known as the originate-to-own model of mortgage lending. Under this approach, the bank that issued the mortgage retained it on its balance sheet for the life of the loan. The mortgage was a valuable asset, generating a predictable stream of income through monthly interest and principal repayments. Because the bank expected to hold the mortgage for decades, it had a strong incentive to carefully evaluate the borrower’s ability to repay. Creditworthiness, employment stability, income history, and down-payment size were central to the lending decision. This alignment of incentives encouraged conservative underwriting and helped contain risk within the banking system.

From Mortgages to a Global Financial Crisis

Over time, banks recognized that the functions of evaluating borrowers and managing large asset portfolios required very different skill sets. This encouraged specialization and led to the originate-to-distribute model, where banks originated loans and then sold them to other financial institutions in exchange for cash. Mortgage brokers focused solely on matching borrowers with loans, earning fees without retaining long-term exposure to credit risk.

Selling mortgages for cash allowed banks to replenish their funds immediately, enabling continuous issuance of new mortgages. Profits increasingly came from origination fees rather than long-term interest income, providing strong incentives to maximize loan volume.

Because banks no longer held mortgages, their incentives to rigorously assess borrower risk weakened. Risky borrowers—including those with unstable employment, poor credit histories, or limited income—were increasingly approved for loans, as risks could be offloaded almost immediately to other institutions.

Financial institutions pooled thousands—even hundreds of thousands—of residential mortgages and transformed them into tradable securities through securitization. Each mortgage carried:

- Individual risk: Specific to the borrower (job loss, illness, default)

- Aggregate risk: Tied to the broader economy (recessions, falling house prices)

Pooling mortgages reduced individual risk but could not eliminate aggregate risk. Securities created from these pools—mortgage-backed securities (MBS) and collateralized debt obligations (CDOs)—were sold worldwide, often perceived as safe due to diversification and AAA credit ratings.

Financial institutions profited by selling these securities at prices higher than the cost of acquiring the underlying mortgages. Investors accepted these prices believing the securities were lower-risk than individual loans.

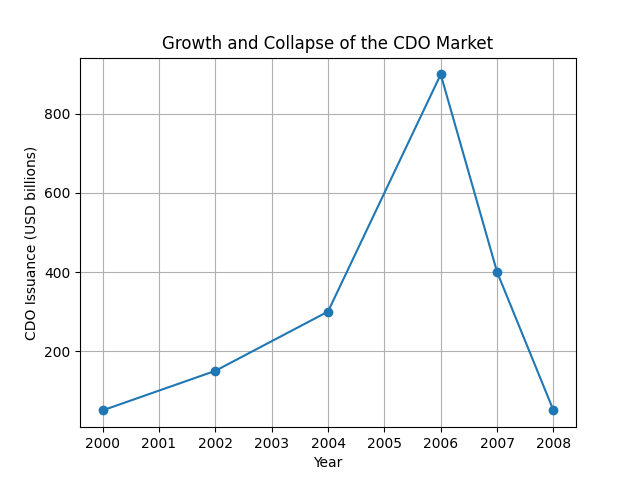

Figure 1: CDO Issuance Over Time

Credit-rating agencies like Moody’s and Standard & Poor’s assigned high ratings to many MBS and CDOs, underestimating true risks due to conflicts of interest, model limitations, and overreliance on diversification. Meanwhile, leveraged shadow banking institutions amplified profits and risk. By 2007, major U.S. investment banks operated with leverage ratios near 28:1, holding only 3.5% capital relative to assets.

Demand for mortgages surged as institutions sought raw material for securitization. Lenders relaxed standards, increasing the share of subprime mortgages from 8% in the early 2000s to 20% by mid-decade. NINJA loans as they came to be refered to, adjustable-rate mortgages with teaser rates, and interest-only loans became common. Borrowers speculated on rising house prices, believing appreciation would offset default risks.

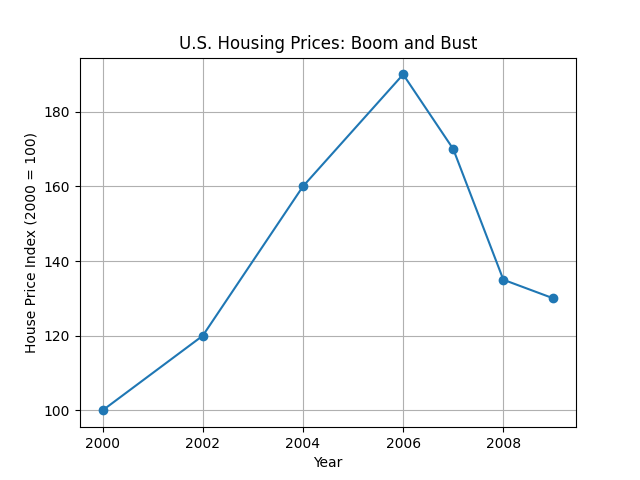

Figure 2: U.S. House Prices (2000–2008)

The Bubble Bursts

Between 2002 and 2006, U.S. house prices rose 8–15% annually. Growth slowed in 2006, and prices fell sharply—down 10% in 2007 and 20% in 2008. Defaults surged, MBS and CDO values declined, and leverage magnified losses.Globalization meant these securities were held worldwide. Banks in the U.S., U.K., and Europe suffered enormous losses, and credit markets froze due to counterparty risk concerns.

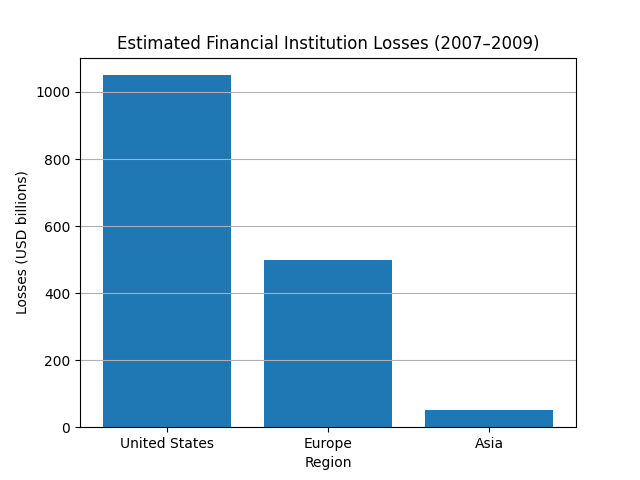

Between 2007 and 2009, financial institutions recorded writedowns of ~$1.6 trillion—roughly Canada’s annual GDP. Stock indices fell 40–50%, and financial stocks lost up to 80% of value.

Figure 3: Global Financial Losses (2007–2009)

The crisis didn’t just affect abstract markets — it toppled major institutions:

- Lehman Brothers — Filed for bankruptcy on September 15, 2008, in what remains the largest bankruptcy in U.S. history. Lehman had large positions in mortgage-backed securities and CDOs that rapidly lost value, depleting capital and triggering its collapse.

- Bear Stearns — One of the first high-profile casualties in 2007 when two of its subprime hedge funds collapsed amid losses on CDO positions, prompting a fire-sale acquisition by JPMorgan Chase.

- Merrill Lynch — Suffered massive losses from holding CDO and other mortgage-related securities. By 2008 it agreed to be purchased by Bank of America as its capital was dangerously eroded.

- American International Group (AIG) — A major insurer that had written credit-default swaps (CDS) on CDOs and could not cover collateral calls as CDO values plunged. The Federal Reserve extended an $85 billion emergency loan to prevent AIG’s failure from cascading throughout the financial system.

Smaller mortgage lenders also disappeared or were absorbed:

- Ameriquest Mortgage — A major subprime originator that shut down in 2007 as investor demand for mortgage products evaporated.

- Washington Mutual — The largest savings and loan association in the U.S. before the crisis, was seized by regulators in 2008 and its assets sold to JPMorgan Chase.

- Countrywide Financial — Once the largest mortgage lender in the U.S., was acquired by Bank of America in 2008 amid soaring loan defaults on its books.

These failures illustrated how leverage, structured products, and off-balance sheet risk could undermine even large, diversified financial firms.

Lessons for Investors.

- Leverage is a double-edged sword: It amplifies returns in good times but destroys capital rapidly when prices fall.

- Diversification does not eliminate systemic risk: Aggregate shocks affect all assets tied to the same macro drivers.

- Incentives matter: Transferring risk away from decision-makers weakens underwriting standards.

- Complexity obscures risk: Hard-to-understand instruments are often mispriced.

- Credit ratings are opinions, not guarantees: Independent analysis is essential.

- Asset prices can deviate from fundamentals: Reversals are inevitable.

- Liquidity can vanish suddenly: Seemingly safe assets can become untradable.

- Policy and regulation shape markets: Low rates and regulatory gaps can fuel excess risk-taking.

- Globalization spreads shocks: Geographic diversification does not insulate against globally synchronized crises.

- Risk-adjusted returns matter more than nominal returns: Sustainable investing requires humility and awareness of uncertainty.

{kind=link}

{kind=link}

{kind=link}

{kind=link}