In financial economics, most theoretical models assume that investors assess risk using the expected utility framework. However, empirical evidence shows that individual behavior and aggregate market outcomes often deviate from the predictions of expected utility maximization. These discrepancies have led researchers to explore alternative decision-making theories. One of the most influential is (cumulative) prospect theory, introduced in 1979 by psychologists Amos Tversky and Daniel Kahneman based on extensive experimental research. Their work, which earned the 2002 Nobel Prize in Economics, is widely regarded as one of the most accurate frameworks for explaining how individuals actually perceive and respond to risk.

One of the most prominent features of prospect theory is loss aversion, which was introduced to explain experimental findings showing that individuals often reject gambles such as a 50–50 chance to gain $110 or lose $100. Kahneman and Tversky (1979) argued that people experience both pleasure and pain directly from gains and losses, and that losses carry greater psychological weight than equivalent gains.

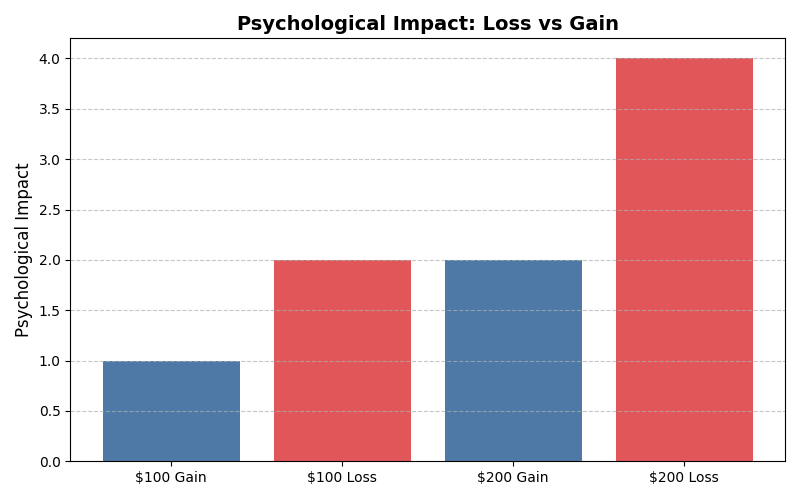

Losses carry roughly twice the psychological weight of equivalent gains, a 2:1 ratio consistently observed across cultures and asset classes.

This asymmetry is evident both on retail trading platforms and in institutional boardrooms, where it influences asset allocation decisions, risk budgeting, and even high-level macro and strategic portfolio choices.

Practical Example of Loss Aversion

Consider an investor offered the following choices:

- 50% chance to gain $1,000

- 50% chance to lose $1,000

From a purely rational, expected-value perspective, the gamble is neutral. Yet most people reject it because the psychological pain of losing $1,000 is roughly twice as intense as the pleasure of gaining $1,000.

To make the investor indifferent — willing to accept the gamble — the potential gain must increase to approximately $2,000:

- 50% chance to gain $2,000

- 50% chance to lose $1,000

At this point, the perceived pleasure from the gain roughly offsets the perceived pain of the loss, reflecting the 2:1 loss aversion ratio documented by Kahneman and Tversky.

How Loss Aversion Impacts Investment Decisions

1. Premature Selling of Winning Investments

Loss-averse investors often sell assets that have appreciated in value too quickly. The motivation is not valuation or fundamentals, but the desire to “lock in” gains and avoid the regret of seeing profits disappear. Over time, this behavior truncates upside and prevents successful investments from compounding fully.

2. Holding Losing Positions Too Long

Investors frequently hold onto losing investments in the hope of breaking even. Realizing a loss converts a paper loss into a psychological one, so investors delay selling even when the investment thesis has deteriorated. Capital becomes trapped in underperforming assets, increasing opportunity cost and portfolio risk.

3. Panic Selling During Market Declines

During periods of heightened volatility or market stress, loss aversion amplifies fear. Temporary drawdowns are perceived as permanent losses, prompting investors to exit positions near market bottoms. When losses are locked in, investors miss subsequent recoveries — often the most powerful phase of market returns.

4. Excessive Risk Aversion After Losses

After experiencing losses, investors tend to become overly conservative. They reduce equity exposure, increase cash holdings, or avoid risk assets altogether — even when expected returns are highest. Portfolios thus become misaligned with long-term objectives, reducing future growth potential.

5. Suboptimal Asset Allocation

Loss aversion influences strategic asset allocation by causing investors to overweight “safe” assets such as cash or short-term bonds. While this may reduce short-term volatility, it increases long-term inflation and longevity risk.

6. Poor Market Timing and Overtrading

Loss-averse investors often react to short-term price movements, trading frequently to avoid losses. This behavior leads to buying high, selling low, and incurring unnecessary transaction costs — resulting in underperformance relative to market benchmarks.

7. Institutional-Level Effects

Loss aversion is not limited to individuals. Institutional investors face career risk, reputational concerns, and benchmarking pressures that reinforce loss-averse behavior. This can result in herd behavior, conservative positioning, and delayed responses to changing fundamentals, leading to missed opportunities and systemic mispricing in financial markets.

Strategies to Overcome Loss Aversion

- Follow a clear investment process: Set asset allocation, rebalancing, and risk rules in advance.

- Separate investments by purpose: Keep long-term goals (retirement) separate from short-term trades.

- Start small and scale gradually: Ease into riskier assets to build comfort with volatility.

- Reframe losses as opportunities: View price drops as chances to invest at lower valuations.

- Set realistic expectations: Accept that short-term losses are normal in market cycles.

- Use stop-loss and take-profit rules: Predefine exit points to avoid emotional trading.

- Limit portfolio monitoring: Avoid checking positions too frequently to reduce stress.

- Diversify your portfolio: Spread risk across assets and markets to soften drawdowns.

- Use behavioral nudges: Automate contributions and rebalancing to stay disciplined.

- Educate and reflect: Learn about behavioral biases and review past decisions.

Loss aversion is a natural part of human psychology, but it does not have to sabotage investment outcomes. By combining process-driven strategies, disciplined frameworks, and mental reframing, investors can turn a potentially costly bias into an edge — capitalizing on opportunities that fear alone would otherwise cause them to miss.

“Markets reward discipline, not emotion.”

{kind=link}